With consumer shopping behaviors in full transition and a crucial holiday season approaching, the marketing industry worldwide continues its efforts to both map and navigate the post-pandemic commerce landscape. New research from OMD Worldwide and Omnicom Commerce Group offers a deep dive into the new retail normal emerging in the wake of the abrupt and extended break in daily retails habits forced by the 2020 lockdown.

The firm’s new report, Future of Commerce | The Why Behind the Buy, looks at consumer behavior and expectations by market, life stage, channel and category to reveal nuances of the retail environment that are emerging in the post-pandemic marketplace—and how marketers can act on them to drive brand growth.

Survey respondents were asked about their attitudes about pandemic-driven changes to their shopping habits, current shopping preferences, expectations for both online and offline shopping experiences, attitudes to returning to shop in city centers and their attitudes towards technology and data-sharing.

The report defines and explores the three most important factors of modern commerce—experience, relevance and ease—defined in the report as Wow, Right, Now.

The report defines and explores the three most important factors of modern commerce—experience, relevance and ease—defined in the report as Wow, Right, Now.

Key findings include:

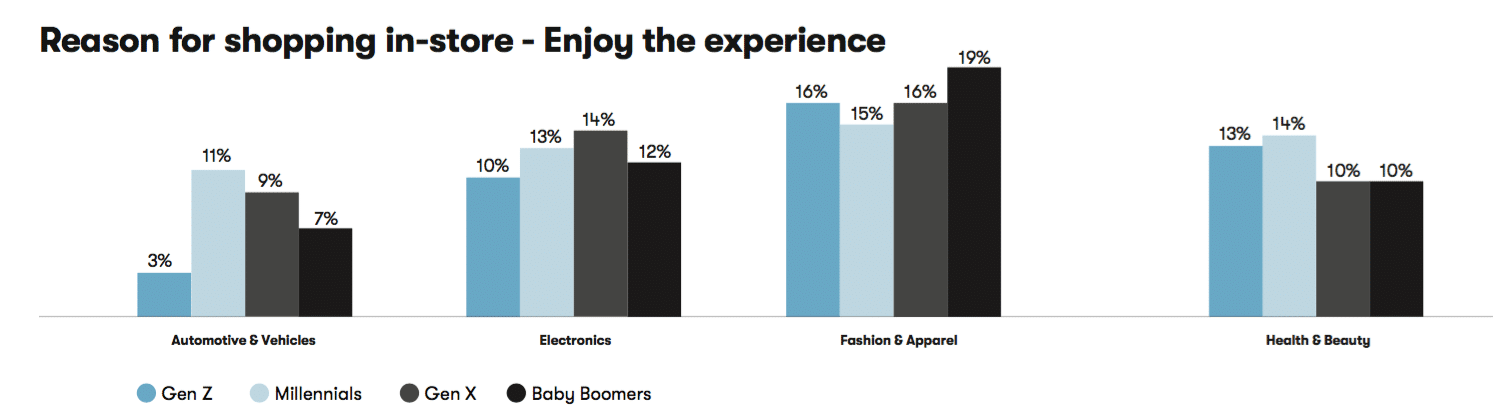

Despite the continued rise of e-commerce, shopping in physical stores still has strong appeal as a lifestyle activity that goes beyond needs fulfilment

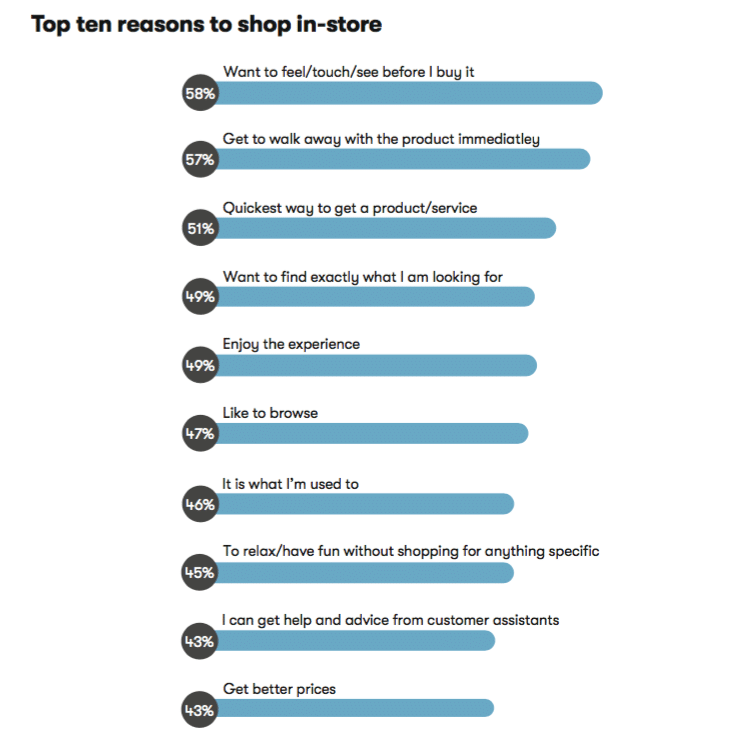

While 39 percent of respondents reporting shopping more frequently online during the pandemic—and 24 percent plan to continue to buy more online in the future—shoppers still appreciate the experience of shopping at physical retail with nearly half of all respondents (49 percent) preferring the experience of shopping in-store and 47 percent enjoying browsing.

A third of respondents highlighted the desire for increased health and safety measures, and 26 percent sited more contactless options a priority for returning to in-store shopping.

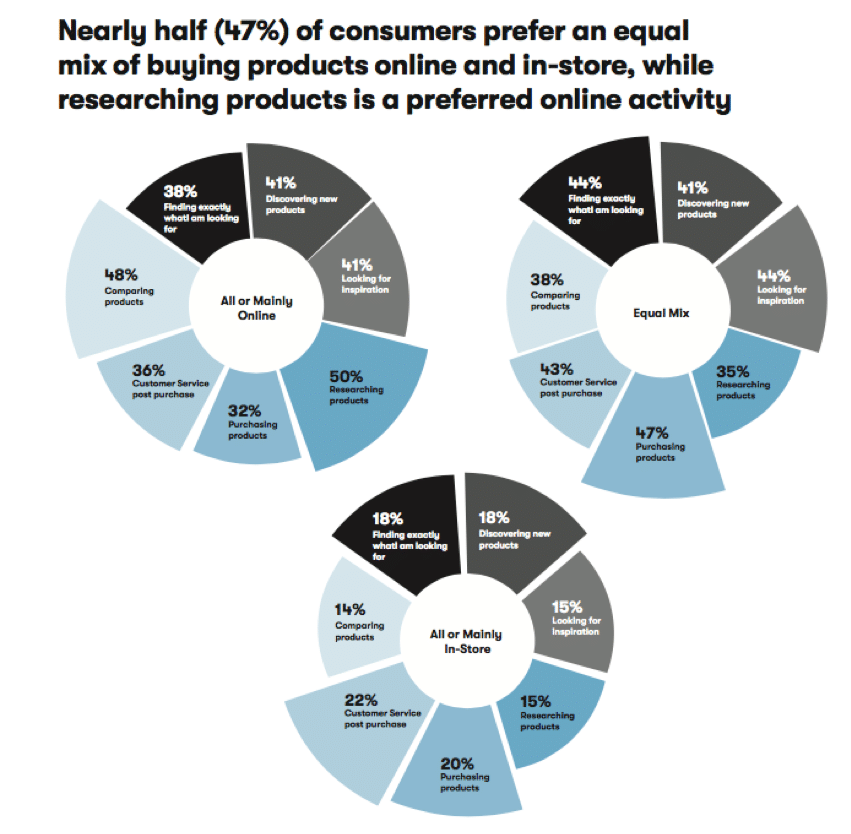

Shoppers are channel fluid: There is no such thing as an online shopper vs. an offline shopper—they want the same thing

Moving forward, nearly half (47 percent) of consumers prefer an equal mix of buying products online and in-store. Shoppers are looking for value, convenience and service when shopping on any channel, but they prioritize them differently. Both are price driven, but one of the primary factors for shopping in store is immediacy.

There is rich opportunity to re-define shopping as a lifestyle with consumers highlighting the desire for a rich combination of socializing, eating & drinking, events and experience

Across all markets, more than half of respondents feel positively about returning, with the USA (55 percent) and China (56 percent) expressing the most confidence. Shopping and dining are the top activities (49 percent) cited as a motivator for returning. However, there is a significant generational divide in net comfort, with desire lowest among Gen Z and Boomers (35 percent) vs Millennials (46 percent) and Gen x (42 percent).

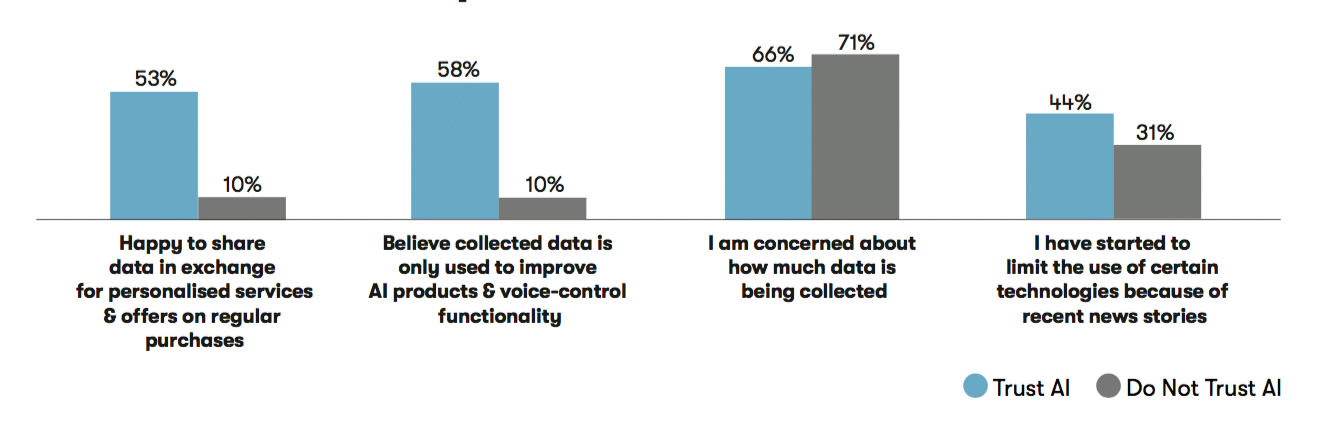

There’s a clear need to better communicate the benefits of technology and data and bridge the trust divide

Even as 74 percent of respondents said AI technology can enhance the shopping experience, 44 percent still don’t trust brands’ motivations for using technology. And 66 percent of consumers are not willing to share any data with at least one type of company.

Those who trust AI believe access to their data will improve their overall customer experience:

Implications for marketers

“The research reconfirms the priority to put consumer behavior and expectations firmly at the forefront of commerce strategy and plan above siloed channels to deliver the seamless end to end experience shoppers clearly expect,” said Sophie Daranyi, CEO of Omnicom Commerce Group and one of the report’s co-authors.

“The research also underscores the imperative for marketers in terms of educating consumers about the data value exchange,” added report co-author and chief product development officer for OMD EMEA Jean-Paul Edwards, in the release. “We need to consider how to elevate data communication to be clearer about the tangible benefits and to establish a relationship based on trust and respect.”

Download the full report here.

The quantitative research encompasses over 4,000 respondents across six global markets (Australia, China, Germany, Spain, the UK and the USA) and was conducted via online surveys from May 11-27, 2021.